While Arconic and PCC Continue Castings Dominance, A New Rival Rises

Before production of Boeing’s 737 MAX was halted and the aircraft type grounded, aerospace manufacturing had only one real bogeyman: investment casting, the metal-forming for engine blades and other aircraft parts.

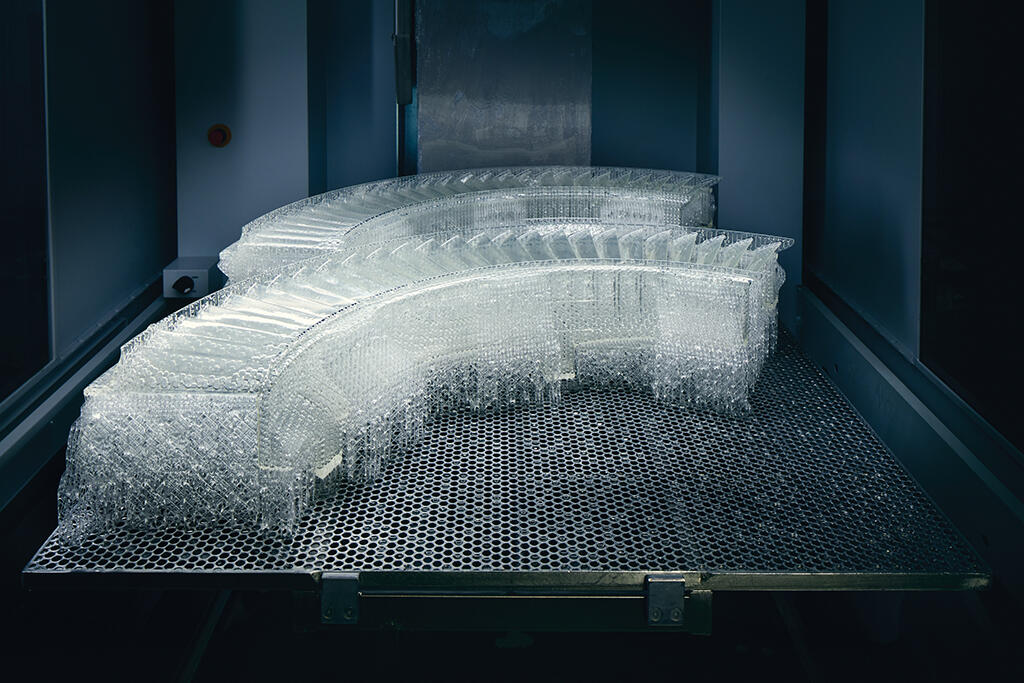

A casual search on YouTube finds numerous videos showing the complexities of castings, whether using the investment or sand processes. The practices require skilled labor experienced both in the science of the 5,000-year-old process as well as the art of applying it to new aerospace programs such as next-generation engine programs.

The learning curve is enormous. On a mature product line, even a high-performing process can see 5% of a production yield thrown away. On new programs, it is not unheard of for half to be discarded in the beginning.

Barriers to entry in the business are high, and industrial capacity remains limited due in part to capital-intensive demands. Castings have been a well-known choke point for growth in commercial aircraft manufacturing and the aftermarket business for years. Some industry executives and advisors have thought that with the MAX slowdown, there might be some relief from recent castings issues. So what has happened?

“Those challenges remain,” says Glenn McDonald, a senior associate at AeroDynamic Advisory, a consulting firm focused on the global aerospace and aviation industries. “It does seem to still be an issue.” Relief for the rest of industry is not expected in the near term; in fact, the situation might become harder for casting customers.

The aerospace castings sector, a roughly $10 billion industry, is dominated by two leading providers: Arconic and Precision Castparts (PCC). There are smaller companies, one of which—Consolidated Precision Products (CPP)—is seen as an up-and-comer. But each has had its own issues, according to industry sources, and are expected to continue to face challenges in meeting demand. At the same time, they also are enjoying their oligopoly positions and raising prices.

For one thing, industry sources say public communication from market leaders Arconic and PCC has become almost nonexistent in recent years. “The communications have shut down on both companies,” says one industry advisor. “It’s hard to get anything.”

PCC was acquired by Berkshire Hathaway, the giant investment group led by Warren Buffett, in January 2016, essentially turning it from a publicly traded and publicly accountable company to a private asset.

Arconic, meanwhile, has been suffering corporate turmoil. In November 2016, Arconic split off from Alcoa but then saw three CEOs in as many years due to disappointing financial results, in part from a failed acquisition, as well as a spat with an activist investor and continued divestitures and restructuring. On Jan. 27, Arconic announced it expects to split into two companies on April 1, an aluminum rolling company and a mostly aerospace-focused business to be called Howmet Aerospace, an homage to the former Howmet Castings bought by Alcoa in 2000.

Yet additional layoffs are possible because of the MAX production halt, according to Arconic Chairman and CEO John Plant. “My expectation is that we will actually be reducing head count,” he told an earnings teleconference, also citing other actions such as partially paid vacation for workers and production shift changes. More information is likely to be forthcoming at a Feb. 25 investor briefing for the new Howmet and Arconic.

Indeed, according to AeroDynamic Managing Director Kevin Michaels, Tier 4 raw material and forging and casting suppliers all will be affected by the MAX halt. Moody’s Investors Service surmised PCC derives more than 10% of its revenue from the MAX.

While PCC’s financial results are unknown, as they are no longer publicly reported, Arconic’s 2019 financial results also are nebulous because there are “lots of moving parts” in the company, executives admit. Still, the to-be Howmet aerospace division reported revenue of $1.7 billion for 2019, up 1% year-over-year. Organic revenue was up 2%, driven by aerospace growth.

A major reason behind the growth is that Arconic continues to raise prices for its products, particularly for aerospace customers. In 2019, the aerospace division—currently called Engineered Products and Forgings—tallied $78 million in price increases compared with 2018.

“We expect favorable pricing to continue,” says Arconic Chief Financial Officer Ken Giacobbe. At the same time, the company finished investing in expansion of aerospace rings and forged wheel production capacity and now expects a return on those investments.

Industry sources say PCC is also raising its prices, yet both companies continue to be challenged delivering to aerospace customers such as engine OEMs. “[There are] the usual things about poor delivery performance and quality issues from Arconic, with all the struggles and operational issues they are going through,” says one source. PCC, meanwhile, is restrained by capacity and “struggling to meet the ramp-up in delivery targets,” particularly for narrowbody engines.

Not surprisingly, the aerospace industry is hungry for more castings providers to both disrupt the top two suppliers and also meet long-term commercial aircraft demands. In turn, many industry observers see hope in CPP, the private-equity-backed Cleveland company that is rolling up sand casting and other assets and working on newer directionally solidified (DS)/single-crystal castings technology.

Founded in 1991, CPP now comprises 19 global facilities manufacturing products for the aerospace, defense and industrial gas turbine markets. CPP makes engine housings, gearboxes, front frames, shrouds, panels, fairings, blades and vanes. Its defense work also includes missile bodies and other structural components to support munitions.

The company was majority-owned by Warburg Pincus from 2011 until last June, when it sold a stake to Berkshire Partners (which is not connected to Berkshire Hathaway). While terms of the deal were not disclosed, Moody’s says CPP is now majority-owned in equal parts by Warburg and Berkshire.

The company is believed to have hit the $1 billion revenue milestone. Commercial aerospace is responsible for two-thirds of annual sales, and the company continues to expand.

“Notwithstanding the company’s small size, we believe there continue to be growth opportunities for CPP (as evidenced by recent business wins and a growing backlog), driven in large part by ongoing engine OEM efforts to minimize and diversify supply chain risk by using dual or triple-sourced suppliers,” Moody’s says in a Dec. 27 report.

CPP further has made “considerable” investment in manufacturing capabilities, particularly around DS/single-crystal technologies, according to credit rating analysts. “We view these investments as having facilitated meaningful content wins on next-generation engine platforms, and the acquisitions of Selmet and Pacific Cast Technologies (both of which add titanium to the company’s product capabilities) are deemed to have helped further improve its competitive standing and support future business wins.,” says Moody’s.

Last July, CPP announced a new advanced manufacturing facility in Euclid, Ohio. It will result in a new 135,000-ft.2 facility and 120 new manufacturing and engineering jobs, according to representatives.

Like Arconic and PCC, CPP holds its proverbial cards close to its vest. But based on what is being said publicly, more competition can be expected. “Our new relationship with Berkshire Partners and ongoing partnership with Warburg Pincus will enable us to further build upon the success we have achieved,” says CPP CEO James Stewart. “Both firms are growth-oriented and have deep expertise in the aerospace and defense sectors.”